Channel checks include speaking with the channel partners like dealers, distributors, suppliers and meeting with competitors. We do this exercise every quarter before the result season to corroborate our thesis on each of our portfolio holdings. Channel checks are done on a pan India basis and not in a specific region; this allows us to understand trends in more granularity.

Key takeaways from channel checks:

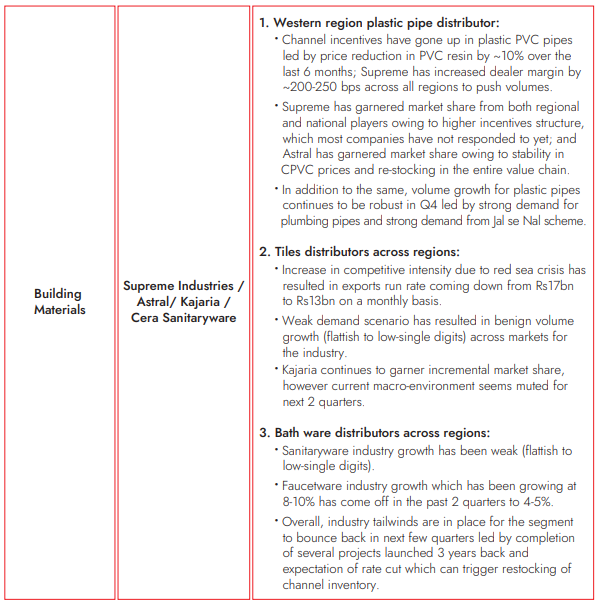

- Persisting weakness in the building material segment led by channel sitting on low inventory due to elevated interest rates and developers focusing on project construction; building material demand comes when the building structure is completed and flats are being prepared for giving possession.

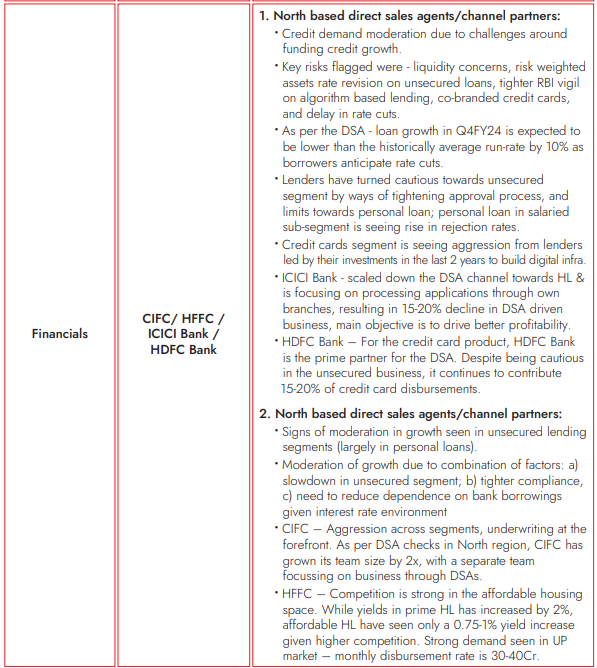

- In financials, banks have become very cautious on unsecured lending led by regulatory tightening. Overall credit growth is also seeing some moderation led by tight liquidity and rising RBI vigilance on algorithm based lending.

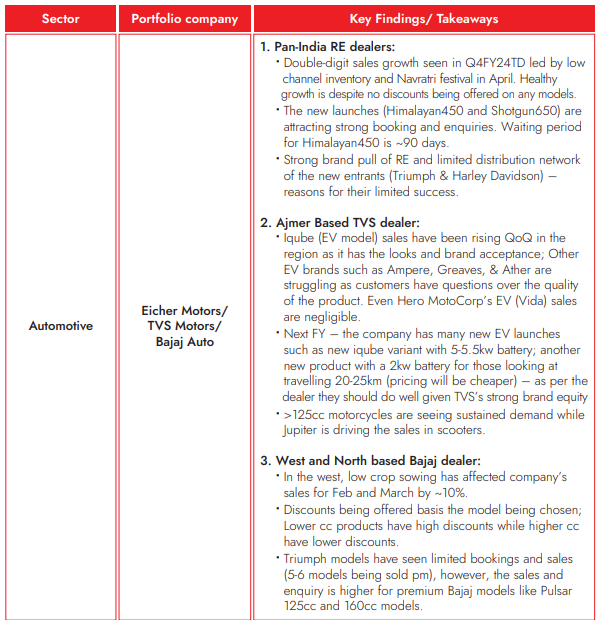

- In 2Ws, Eicher continues to report double-digit volume growth led by success in new product launches and rising demand due to upcoming Navratri festival in North India. TVS continues to see double digit growth in its EV portfolio led by success in iqube series.

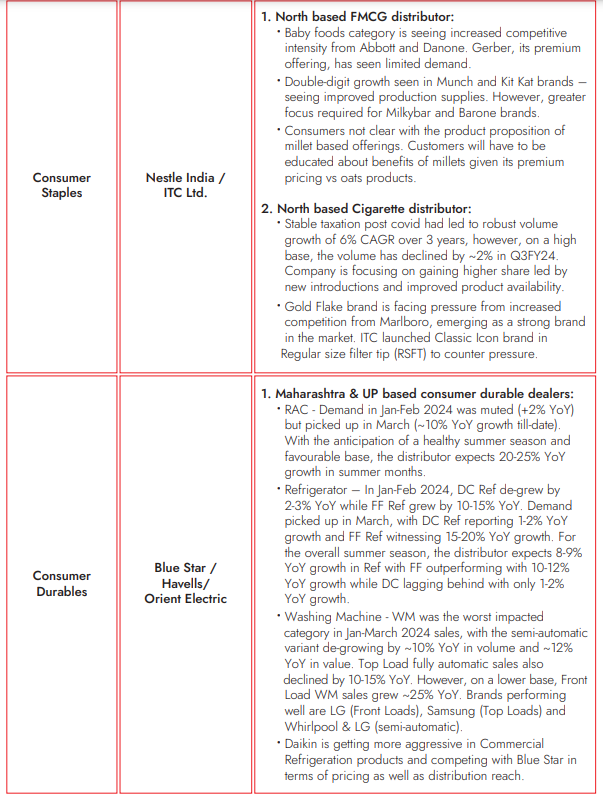

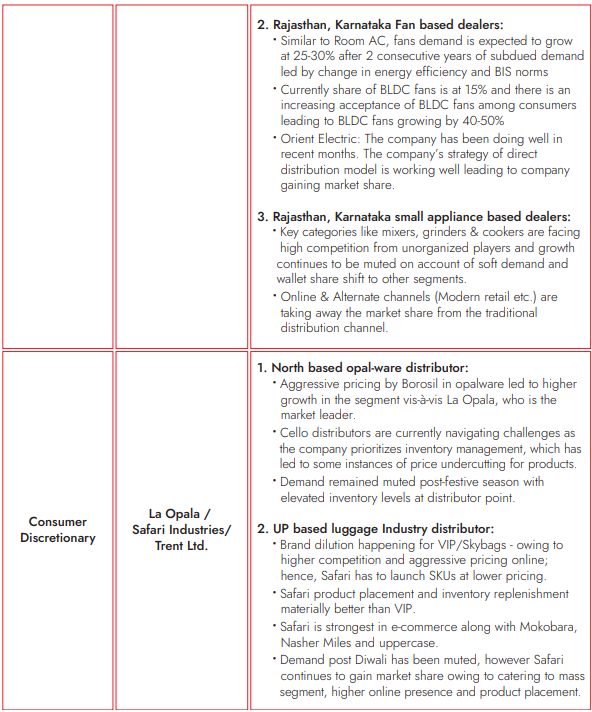

- Fans is seeing strong demand led by low channel inventory and rising acceptance of BLDC post the change in emission norms. Consumer durables demand continues to remain sluggish with washing machine and refrigerator reporting flat to negative volume growth; ACs also saw flattish volume growth in Jan/Feb, March however saw 10% volume growth led by delayed summer.

- Stable taxation post covid had led to robust cigarette volume CAGR of 6% over 3 years, however, on a high base, the volume has declined by ~2% in Q3FY24.

- Luggage and apparel demand has moderated due to seasonally weak quarter due to lower marriages.

KEY FINDINGS FROM CHANNEL/INDUSTRY INTERACTIONS:

CONCLUSION

We expect 4Q to be a muted quarter for our portfolio companies given the persisting weakness in building material/apparel/luggage/consumer staples and lower credit growth in financials. However, we remain optimistic about FY25. The cut in interest rates could act as a big catalyst for demand revival across sectors given the ~250bps increase in interest rates over the last 2 years has led to higher working capital requirements. Aggressive price cuts by several companies could trigger deflationary trends in key raw materials, which, in turn, can boost rural demand, especially in consumer discretionary segments. Lastly, we await the Union budget announcements, which are likely to focus on private capex and fiscal prudence. Completion of several under-construction projects should revive building materials demand.

AMBIT COFFEE CAN PORTFOLIO

At Coffee Can Portfolio, we do not attempt to time commodity/investment cycles or political outcomes and prefer resilient franchises in the retail and consumption-oriented sectors. The Coffee Can philosophy has an unwavering commitment to companies that have consistently sustained their competitive advantages in core businesses despite being faced with disruptions at regular intervals. As the industry evolves or is faced with disruptions, these competitive advantages enable such companies to grow their market shares and deliver long-term earnings growth.

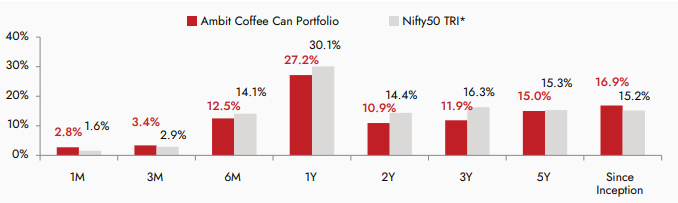

Exhibit 1: Ambit Coffee Can Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is March 6, 2017; Returns as of March 31st 2024; All returns are post fees and expenses; Returns above 1 year are annualized; Note: Returns prior to Apr’19 are returns of all the Pool accounts excluding non-aligned portfolio, and returns post Apr’19 is based on TWRR returns of all the pool accounts. *Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio and the same is reported to SEBI.

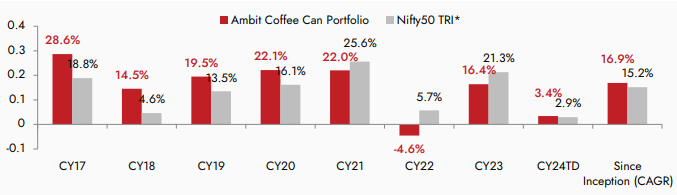

Exhibit 2: Ambit’s Coffee Can Portfolio calendar year performance

Source: Ambit; Portfolio inception date is March 6, 2017; Returns as of March 31st 2024; All returns are post fees and expenses. Note: Returns prior to Apr’19 are returns of all the Pool accounts excluding non-aligned portfolio, and returns post Apr’19 is based on TWRR returns of all the pool accounts. *Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio and the same is reported to SEBI.

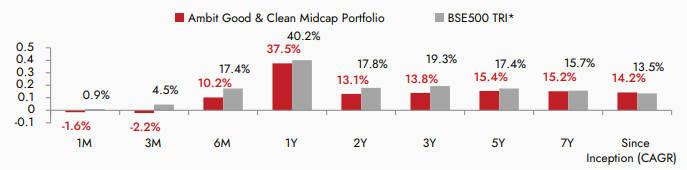

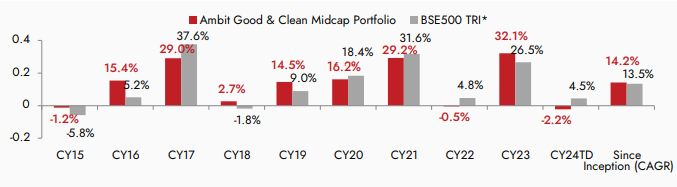

AMBIT GOOD & CLEAN MIDCAP PORTFOLIO

Ambit's Good & Clean strategy provides long-only equity exposure to Indian businesses that have an impeccable track record of clean accounting, good governance, and efficient capital allocation. Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts, while our proprietary ‘greatness’ framework helps identify efficient capital allocators with a holistic approach for consistent growth. Our focus has been to deliver superior risk-adjusted returns with as much focus on lower portfolio drawdown as on return generation. Some salient features of the Good & Clean strategy are as follows:

- Process-oriented approach to investing: Typically starting at the largest 500 Indian companies, Ambit's proprietary frameworks for assessing accounting quality and efficacy of capital allocation help narrow down the investible universe to a much smaller subset. This shorter universe is then evaluated on bottom-up fundamentals to create a concentrated portfolio of no more than 20 companies at any time.

- Long-term horizon and low churn: Our holding horizons for investee companies are 3-5 years and even longer with annual churn not exceeding 15-20% in a year. The long-term orientation essentially means investing in companies that have the potential to sustainably compound earnings, with these compounding earnings acting as the primary driver of investment returns over long periods.

- Low drawdowns: The focus on clean accounting and governance, prudent capital allocation, and structural earnings compounding allow participation in long-term return generation while also ensuring low drawdowns in periods of equity market declines.

Exhibit 3: Ambit’s Good & Clean Midcap Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is March 12, 2015; Returns as of March 31st 2024; All returns above 1 year are annualized. Returns are net of all fees and expenses. *BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Midcap Portfolio and the same is reported to SEBI.

Exhibit 4: Ambit’s Good & Clean Midcap Portfolio calendar year performance

Source: Ambit; Portfolio inception date is March 12, 2015; Returns as of March 31st 2024. Returns are net of all fees and expenses. *BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Midcap Portfolio and the same is reported to SEBI.

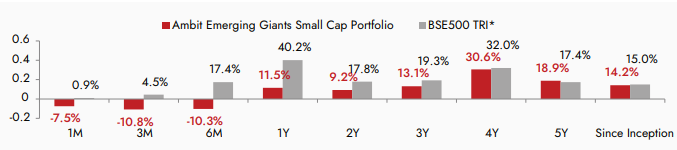

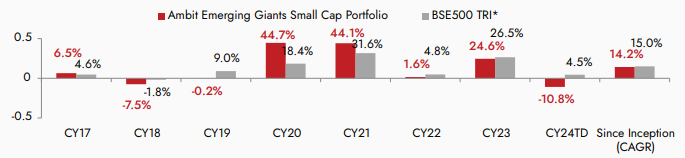

AMBIT EMERGING GIANTS SMALL CAP PORTFOLIO

Small caps with secular growth, superior return ratios and no leverage – Ambit's Emerging Giants portfolio aims to invest in small-cap companies with market-dominating franchises and a track record of clean accounting, governance and capital allocation. The fund typically invests in companies with market caps less than Rs4,000cr. These companies have excellent financial track records, superior underlying fundamentals (high RoCE, low debt), and the ability to deliver healthy earnings growth over long periods of time. However, given their smaller sizes, these companies are not well discovered, owing to lower institutional holdings and lower analyst coverage. Rigorous framework-based screening coupled with extensive bottom-up due diligence led us to a concentrated portfolio of 15-16 emerging giants.

Exhibit 5: Ambit Emerging Giants Small Cap Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is December 1, 2017; Returns as of March 31st 2024; All returns above 1 year are annualized. Returns are net of all fees and expenses. *BSE 500 TRI is the selected benchmark for the Ambit Emerging Giants Small Cap Portfolio and the same is reported to SEBI.

Exhibit 6: Ambit Emerging Giants Small Cap Portfolio calendar year performance

Source: Ambit; Portfolio inception date is December 1, 2017; Returns as of March 31st 2024. Returns are net of all fees and expenses. *BSE 500 TRI is the selected benchmark for the Ambit Emerging Giants Small Cap Portfolio and the same is reported to SEBI.

AMBIT TenX PORTFOLIO

Ambit TenX Portfolio gives investors an opportunity to participate in the India growth story as the Indian GDP heads towards a US$10tn mark over the next 12-15 years. Mid and Small corporates are expected to be the key beneficiaries of this growth. The portfolio intends to capitalize on this opportunity by identifying and investing in primarily mid & small cap companies that can grow their earnings 10x over the same period implying 18-21% CAGR. Key features of this portfolio would be as follows:

- Longer-term approach with a concentrated portfolio: Ideal investment duration of >5 years with 15-20 stock.

- Key driving factors: Low penetration, strong leadership, light balance sheet

- Forward-looking approach: Relying less on historical performance and more on future potential while not deviating away from the Good & Clean philosophy.

- No Key-man risk: Process is the Fund Manager

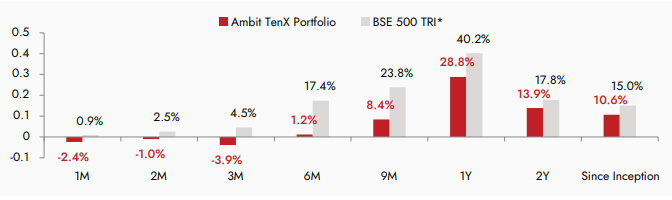

Exhibit 7: Ambit TenX Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is December 13, 2021; Returns as of March 31st 2024; Returns are net of all fees and expenses *BSE 500 TRI is the selected benchmark for the Ambit TenX Portfolio and the same is reported to SEBI.

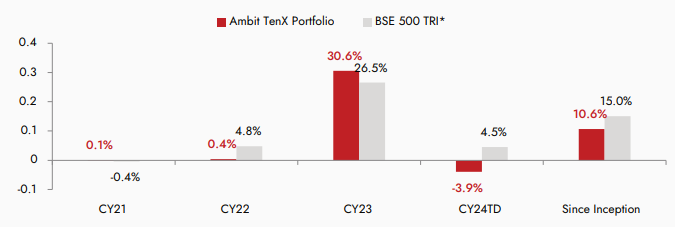

Exhibit 8: Ambit TenX Portfolio calendar year performance

Source: Ambit; Portfolio inception date is December 13, 2021; Returns as of March 31st 2024. Returns are net of all fees and expenses *BSE 500 TRI is the selected benchmark for the Ambit TenX Portfolio and the same is reported to SEBI.